Introduction

Employee welfare expenses constitute a significant component of business expenditure. From an accounting perspective, such expenses are governed by Accounting Standard 15 (AS 15) – Employee Benefits, which prescribes the recognition, measurement, and disclosure of employee benefit obligations in financial statements. From a taxation perspective, deductions for employee welfare contributions are regulated under Section 29 of the Income-tax Act, 2025, which determines the allowability of such expenses while computing business income.

While AS 15 focuses on the accounting recognition and measurement of employee benefits, Section 29 governs the tax deductibility of employer contributions towards employee welfare funds. Understanding the interrelationship between these provisions is essential for accurate financial reporting and tax compliance.

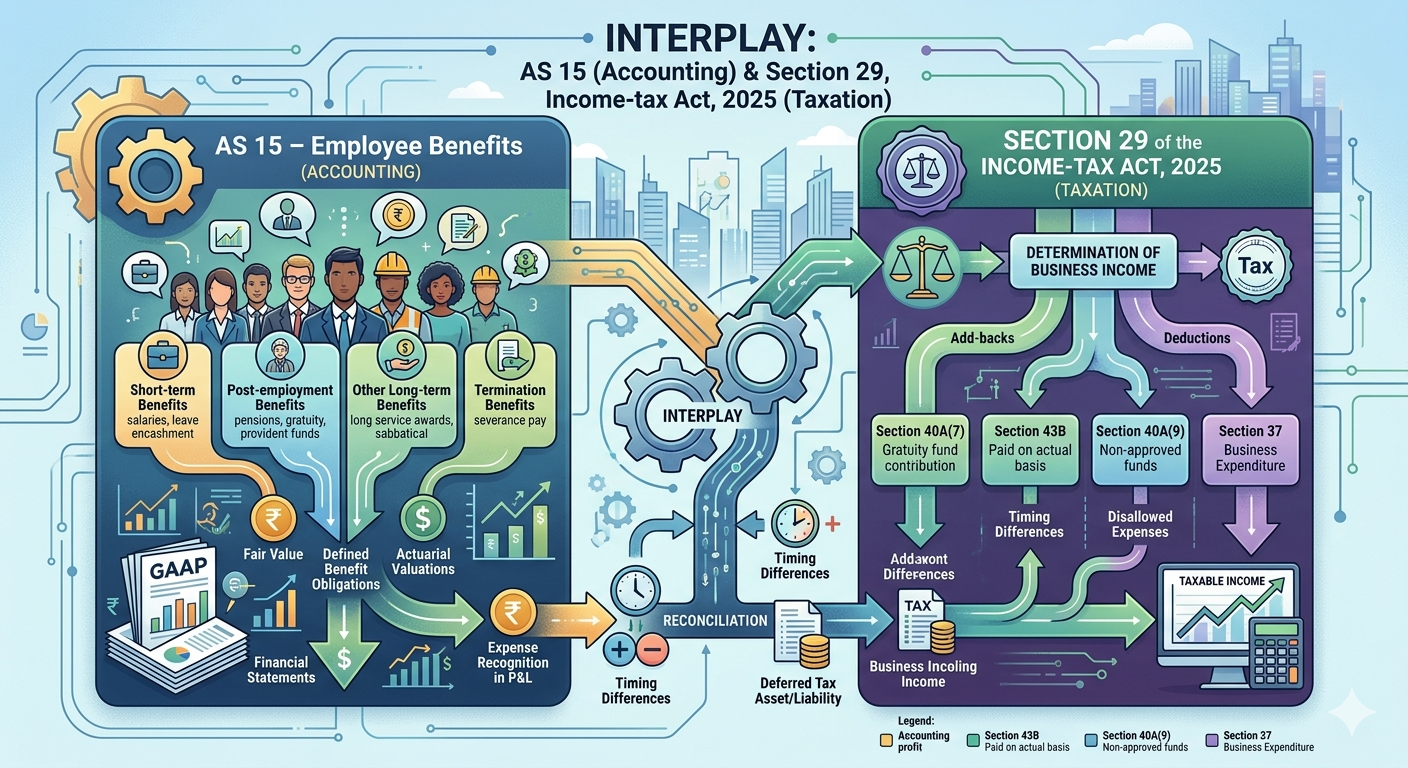

1. Accounting Standard (AS) 15 – Employee Benefits

Objective of AS 15

AS 15 prescribes the accounting treatment and disclosure requirements for employee benefits provided by an enterprise to its employees. The standard ensures that enterprises recognize the liability and expense related to employee services in the period in which the services are rendered.

Employee benefits represent all forms of consideration given by an enterprise in exchange for services rendered by employees.

2. Applicability – Which Entities Must Follow AS 15?

AS 15 is applicable to all enterprises that prepare financial statements in accordance with Accounting Standards issued by the Institute of Chartered Accountants of India (ICAI).

The standard applies to:

- Companies preparing financial statements under the Companies Act

- Non-corporate entities following ICAI Accounting Standards

- Enterprises employing full-time, part-time, temporary, or managerial personnel.

The applicability may differ depending on the classification of entities such as Level I, II, III, or IV enterprises based on turnover and listing status.

3. Types of Employee Benefits under AS 15

AS 15 classifies employee benefits into four categories, each with different accounting requirements:

- Short-Term Employee Benefits

Benefits payable within 12 months after the end of the period in which employees render service.

Examples include:

- Salaries and wages

- Bonus and profit sharing

- Leave encashment (short-term)

- Medical benefits

- Non-monetary benefits such as housing or subsidised goods.

Such benefits are generally recognized as an expense in the period in which the employee renders the related service.

- Post-Employment Benefits

Benefits payable after completion of employment.

Examples:

- Gratuity

- Pension

- Post-retirement medical benefits

- Provident fund.

These benefits are categorized as:

- Defined Contribution Plans

- Defined Benefit Plans

c. Other Long-Term Employee Benefits

Benefits not payable within twelve months after service but not classified as post-employment benefits.

Examples:

- Long service leave

- Long service awards

- Long-term disability benefits.

d. Termination Benefits

Benefits payable as a result of termination of employment.

Examples include:

- Voluntary retirement compensation

- Retrenchment compensation.

4. Accounting Treatment of Employee Benefits under AS 15

The accounting treatment depends on the category of benefit.

Short-Term Benefits

- Recognized as expense in the profit and loss account when employees render service.

- Any unpaid amount is recognized as liability.

Defined Contribution Plans

Examples: Provident fund, superannuation fund.

Accounting treatment:

- Employer contribution is recognized as an expense in the period in which the employee renders service.

- No further liability arises once the contribution is made.

Defined Benefit Plans

Examples: Gratuity and pension.

Accounting treatment involves:

- Determination of present value of defined benefit obligation

- Deduction of fair value of plan assets

- Recognition of actuarial gains/losses and service cost.

This often requires actuarial valuation to determine the present value of the obligation.

5. Deductions Related to Employee Welfare under Section 29 – Income-tax Act, 2025

Section 29 of the Income-tax Act, 2025 deals with deductions available to employers for contributions made towards employee welfare schemes.

The deduction is allowed while computing income under the head “Profits and Gains of Business or Profession.”

5.1 Who Can Claim Deduction under Section 29?

The deduction can be claimed by an assessee who is an employer, in respect of contributions made for the welfare of employees.

5.2 Deduction under Section 29(1)(a)

Employers are allowed deduction for contributions made towards:

- Recognised Provident Fund

- Approved Superannuation Fund

The deduction is allowed subject to prescribed limits and conditions regarding recognition and approval of such funds.

5.3 Deduction under Section 29(1)(b)

Deduction is allowed for contributions made by the employer towards a pension scheme.

Maximum allowable deduction:

Up to 14% of the employee’s salary (including dearness allowance but excluding other allowances and perquisites).

5.4 Deduction for Contribution to Gratuity Fund

Yes, deduction is allowed for:

- Contributions made to an approved gratuity fund created exclusively for the benefit of employees under an irrevocable trust.

However:

- No deduction is allowed for mere provision for gratuity on retirement or termination, unless it relates to gratuity that has become payable during the tax year.

6. Interlinking Between AS 15 and Section 29

Although both provisions deal with employee benefits, their objectives differ.

Key difference:

Under AS 15, enterprises must recognize employee benefit obligations on accrual basis, whereas Section 29 allows tax deduction only when conditions prescribed under the Income-tax Act are satisfied.

7. Practical Implications

The difference between accounting recognition and tax deduction may lead to:

- Timing differences

- Deferred tax adjustments

- Disallowance of provisions for tax purposes

- Compliance requirements for approved funds

For example:

- Gratuity liability recognized under AS 15 may not be fully deductible under Section 29 unless paid to an approved gratuity fund.

Conclusion

Employee benefit obligations play a crucial role in both financial reporting and tax computation. While AS 15 ensures accurate recognition and measurement of employee benefit liabilities, Section 29 of the Income-tax Act, 2025 provides the framework for tax deductibility of employer contributions towards employee welfare schemes.

Therefore, organizations must carefully align their accounting policies under AS 15 with tax provisions under Section 29 to ensure compliance, avoid disallowances, and maintain transparency in financial reporting.

Disclaimer: This article is for academic and informational purposes only. It’s not legal advice or a substitute for professional judgment. Readers should verify provisions, check updates, and seek specific advice. No liability for errors or reliance.