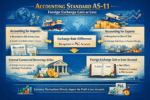

In today’s globalized economy, businesses frequently engage in cross-border transactions. Whether you are importing raw materials or exporting finished goods, fluctuations in foreign currency exchange rates can significantly impact your financial statements. Accounting Standard 11 (AS-11) provides the essential framework for recognizing these gains and losses.

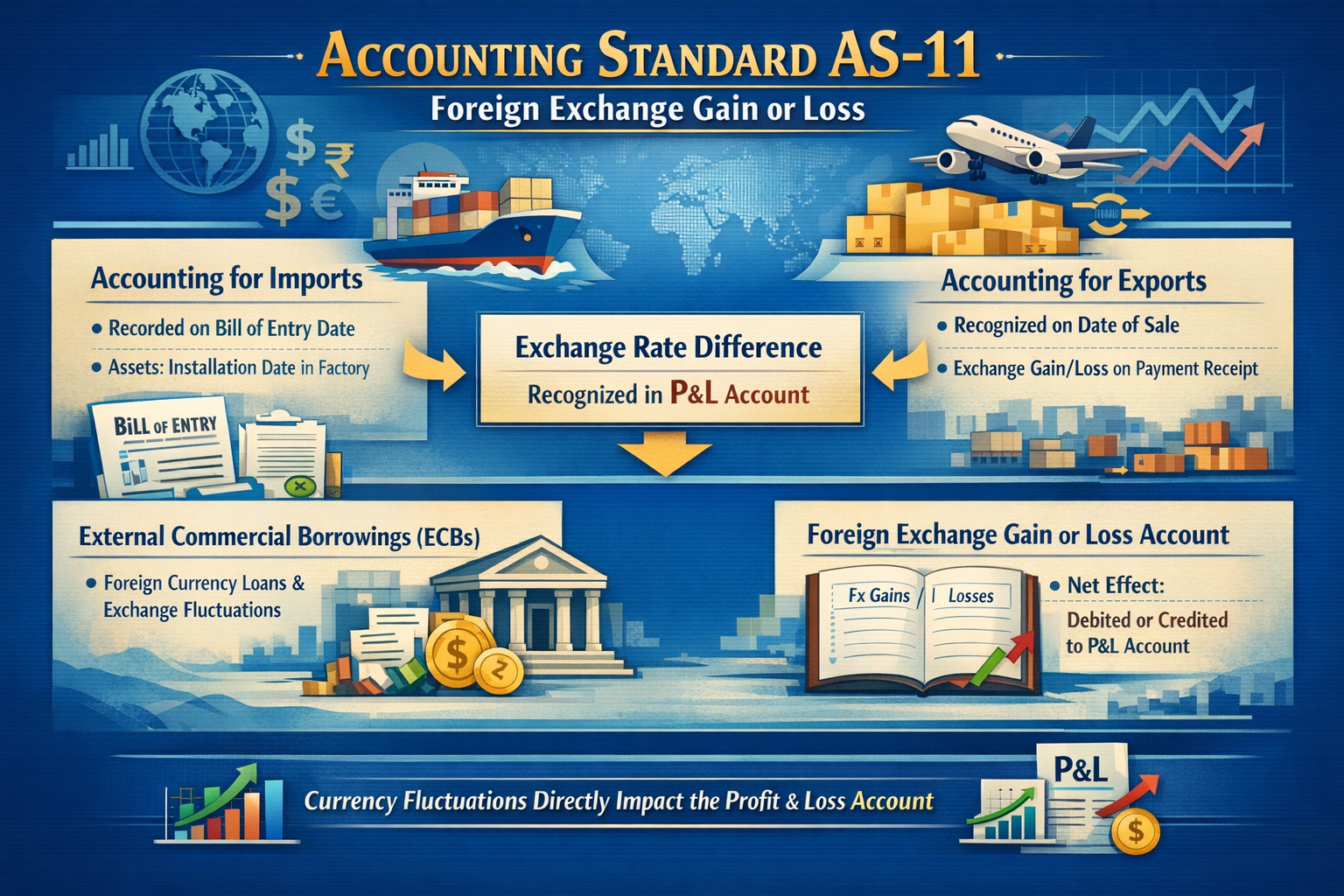

1. Accounting for Imports

When a business imports goods or services, the transaction initiation (such as issuing a purchase order) is not the point of financial recognition. Instead, the standard focuses on the following:

- Regular Expenses (Raw Materials/Services): The date of the Bill of Entry is typically used to recognize the goods as purchases and record the liability in the books.

- This is when the goods are cleared from customs and considered under your control.

- Asset Purchases: For fixed assets, the date of installation in the factory is a critical milestone, as this is when depreciation begins to be charged.

Recognition of Gain/Loss

The foreign exchange gain or loss is calculated based on the difference between the exchange rate on the date of recognition (invoice/bill of entry) and the date of actual payment. AS-11 guides that this difference should be charged directly to the Profit and Loss (P&L) account as revenue income or expense.

2. Accounting for Exports

For businesses selling goods or services abroad, the logic remains consistent but applies to income and receipts:

- Recognition Date: The export is recognized on the date of sale, which is determined by the dispatch of goods (via sea or air).

- Settlement: The difference between the exchange rate on the date of the invoice and the date the payment is actually received constitutes the exchange gain or loss.

3. External Commercial Borrowings (ECBs)

If a company takes out foreign currency loans, such as ECBs, these are treated as liabilities. Similar to trade transactions, any fluctuations in the exchange rate affecting these liabilities must be accounted for according to the standard.

4. The “Foreign Exchange Gain or Loss” Account

All differences arising from these transactions are funneled into a nominal account titled “Foreign Exchange Gain or Loss”.

- Net Effect: At the end of the period, the net balance of this account is either debited or credited to the P&L account.

Conclusion

AS-11 ensures that the volatility of global currencies is transparently reflected in a company’s financial health. By accurately pinning the recognition dates for imports, exports, and assets, businesses can maintain a clear and compliant record of their international financial dealings

Disclaimer: This article is for academic and informational purposes only. It’s not legal advice or a substitute for professional judgment. Readers should verify provisions, check updates, and seek specific advice. No liability for errors or reliance.