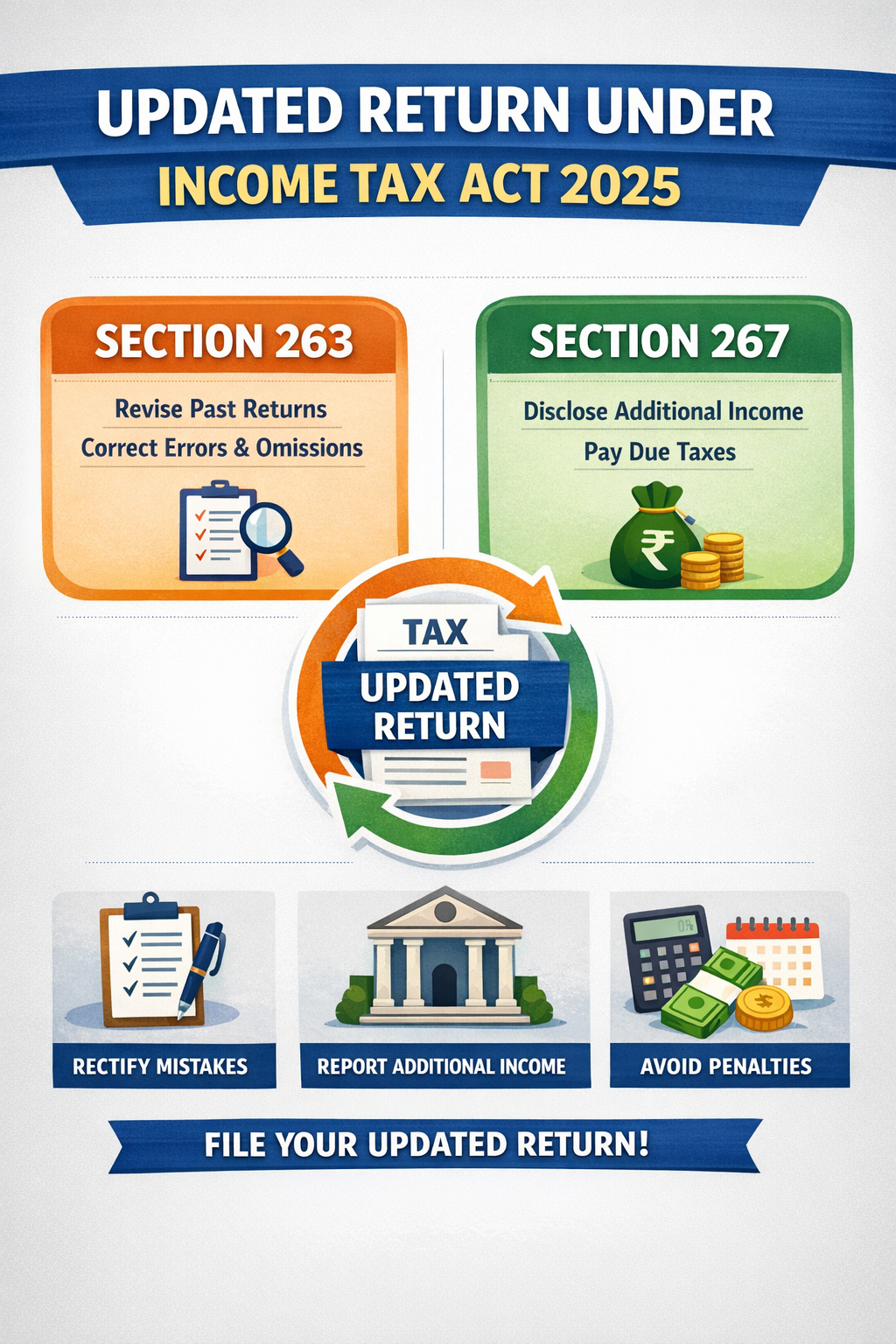

Section 139(8A) under old Act and Corresponding 263(6) and 267 under new act

1. Introduction

The Indian tax administration has increasingly emphasized voluntary compliance and transparency in tax reporting. In line with this objective, the concept of an Updated Return was introduced under Section 139(8A) of the Income-tax Act, 1961 to provide taxpayers with an opportunity to correct omissions or errors in previously filed returns or to declare income that was inadvertently left out.

Subsequent amendments through the Finance Act, 2025 have further strengthened this framework by extending the time limit for filing updated returns, thereby encouraging taxpayers to voluntarily disclose additional income and regularize their tax affairs.

This provision reflects a shift in tax policy—from punitive enforcement to a compliance-oriented approach that allows taxpayers to rectify mistakes before enforcement action is initiated.

2. What is an Updated Return under the Income Tax Act, 2025?

A taxpayer can use an Updated Return to fix mistakes or add income that wasn’t reported in the Income Tax Return.

According to Section 139(8A) of the Income-tax Act, 1961, any taxpayer can file an updated return for a relevant assessment year in order to:

• Declare extra income that wasn’t disclosed before,

• rectify mistakes or omissions in returns previously filed, or

• File a return even if you didn’t file one previously.

File it with Form ITR-U and the right ITR form.

The goal of this provision is to encourage people to pay their taxes on time by letting them fix mistakes and report income without having to wait for the department to do something.

3. Time Limit for Filing an Updated Return

Originally, the time limit for filing an updated return was 24 months from the end of the relevant assessment year. However, the Finance Act, 2025 extended this period to 48 months, thereby providing taxpayers with a longer window to correct their tax filings.

Accordingly, an updated return can now be filed:

Within 48 months from the end of the relevant assessment year.

For example:

| Assessment Year | Last date to file Updated Return |

| AY 2023-24 | 31 March 2028 |

| AY 2024-25 | 31 March 2029 |

However, filing an updated return requires payment of additional tax, which increases depending on the delay in filing.

4. Who is Eligible to File an Updated Return?

The law allows any person to file an updated return, whether or not they have previously filed a return under:

- Section 139(1) – Original return

- Section 139(4) – Belated return

- Section 139(5) – Revised return

Thus, the following taxpayers may file an updated return:

- Individuals

- Hindu Undivided Families (HUFs)

- Firms

- Companies

- Any other person assessable under the Act

A taxpayer may file an updated return for their own income or the income of another person for whom they are assessable (for example, representative assessees).

However, the law also prescribes certain restrictions, and an updated return cannot be filed if:

- The return results in a loss.

- The return reduces the tax liability already determined.

- The return results in a refund or increases an existing refund.

These restrictions ensure that the provision is used primarily for voluntary disclosure of additional income, rather than for obtaining tax benefits.

5. Can an Assessee File an Updated Return After the Time Limit for a Revised Return Has Expired?

Yes.

An assessee can file an updated return even after the expiry of the time limit for filing a revised return.

Normally:

- A revised return under Section 139(5) can be filed only up to three months before the end of the relevant assessment year or before completion of assessment, whichever is earlier.

However, if this time limit has expired, the taxpayer still has the option to file an updated return under Section 139(8A) within the extended time limit of 48 months from the end of the relevant assessment year.

Therefore, the updated return acts as a last opportunity for taxpayers to declare additional income and correct earlier omissions before the tax authorities initiate proceedings.

This mechanism allows taxpayers to regularize their tax position by paying:

- Due tax

- Interest

- Additional tax prescribed under Section 140B.

6. Additional Tax Liability on Updated Return

While the updated return provides flexibility, it also imposes an additional tax burden as a deterrent against delayed compliance.

The additional tax payable depends on the time of filing:

| Period of filing | Additional tax |

| Up to 12 months | 25% of tax and interest |

| 12–24 months | 50% |

| 24–36 months | 60% |

| 36–48 months | 70% |

This progressive structure encourages taxpayers to regularize errors at the earliest possible stage.

7. Practical Significance of Updated Returns

The updated return mechanism serves several practical purposes:

1. Encourages voluntary disclosure

Taxpayers can disclose previously omitted income without waiting for departmental notices.

2. Reduces litigation

By enabling self-correction, the provision helps reduce disputes between taxpayers and the tax department.

3. Strengthens tax administration

It improves revenue collection while promoting transparency.

4. Provides compliance flexibility

Taxpayers who discover errors after the revision deadline can still rectify their returns.

8. Conclusion

The introduction and expansion of the updated return facility represent a progressive step in India’s tax administration. By allowing taxpayers to correct mistakes and voluntarily disclose additional income, Section 139(8A) of the Income-tax Act, 1961 fosters a cooperative tax environment based on trust and compliance.

With the extension of the filing window to 48 months under the Finance Act, 2025, taxpayers now have a broader opportunity to rectify errors and align their tax filings with the law. However, the additional tax burden associated with delayed disclosure underscores the importance of timely and accurate reporting of income.

In essence, the updated return provision serves as a “second chance” for taxpayers—one that balances compliance flexibility with fiscal responsibility.

Disclaimer: This article is for academic and informational purposes only. It’s not legal advice or a substitute for professional judgment. Readers should verify provisions, check updates, and seek specific advice. No liability for errors or reliance.